Some deliveries may take a little longer than usual due to regional shipping conditions.

DOWNLOAD THE APP

Customer Services

Copyright © 2025 Desertcart Holdings Limited

DOWNLOAD THE APP

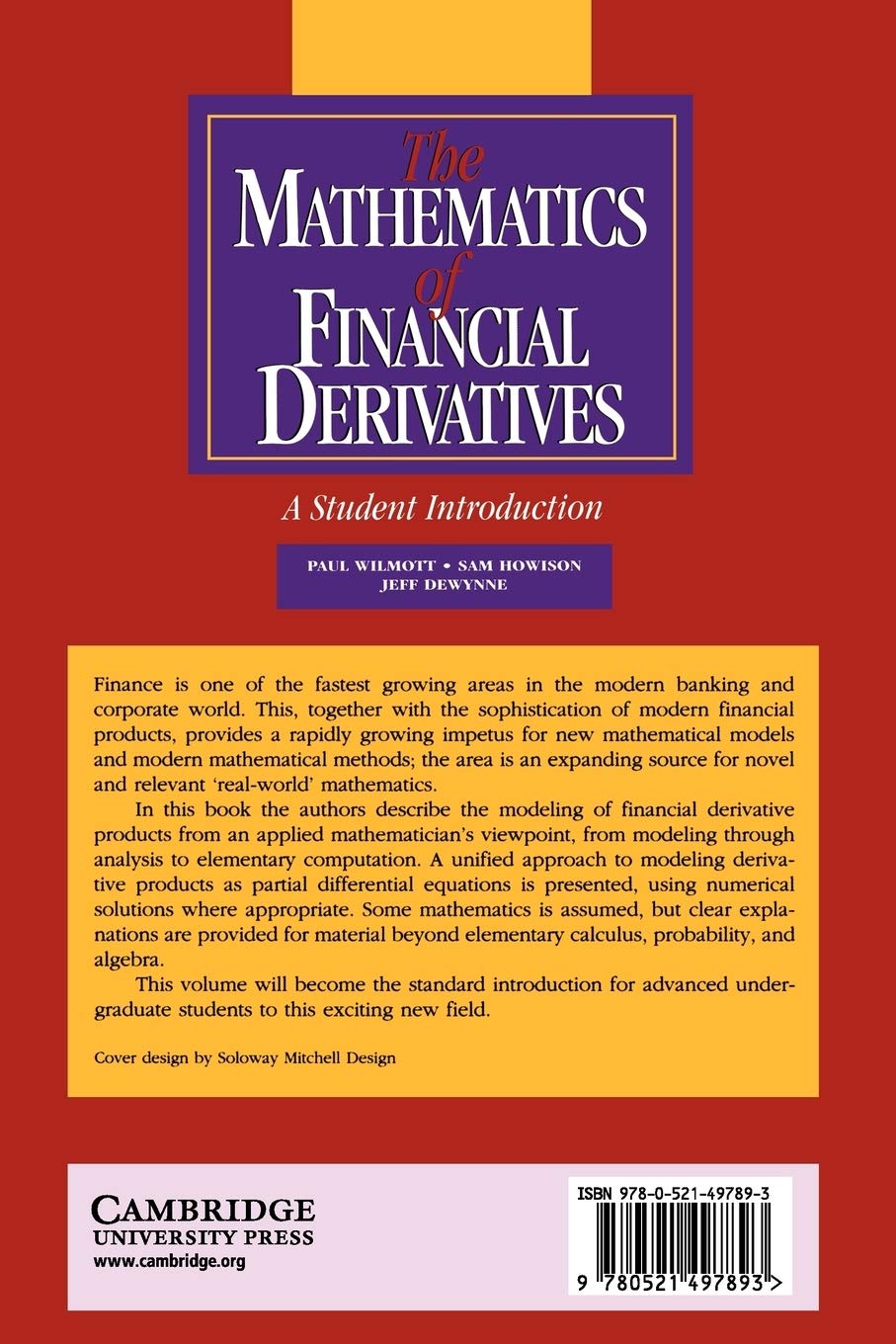

desertcart.com: The Mathematics of Financial Derivatives: A Student Introduction: 9780521497893: Wilmott, Paul, Howison, Sam, Dewynne, Jeff: Books Review: Five Stars - It's great as expected. Review: A good introduction to the PDE approach - Contrary to what many readers believe, this book explains the pricing of derivatives much better than Hull. Hull gives an overview of the mechanics and properties of the derivative pricing industry, along with its pricing methodologies, and this book provides an in depth method to one of the pricing methods. Financial derivatives can be priced by a wide range of methodologies, among some the elegant equivalent martingale measure approach (or risk-neutral pricing), replication, multinomial tree approximation, Monte Carlo simulation, partial differential equations etc etc. This book gives an excellent introduction, and an insight to the PDE approach. Although being a big fan of the Girsanov-change-of-measure method myself, these analytical methods often fail in the valuation of highly complex derivatives like the exotics. Pricing americans prove to be hard and inefficient too, even with simulation and the risk-neutral approach. This is where PDE methods come in. Since most derivatives (or term structures) have a PDE describing its evolution, solving the PDE seems to be a good (or sometimes the best) way, no matter how complex the derivative can get. PDEs on the other hand, have very robust and easy methods for solving. Therefore, this book brings the reader through basic PDE solving methods, analytical solutions, techniques for fast and efficient numerical approximations as well as rigorous technical explanations for some of the mathematics of partial differential equations (which arise in the financial industry). The authors are famous for their research in the field of Industrial and Applied Mathematics, and this book continues to be a classic for undergraduates in mathematics in Oxford. If you want to have an overview of the pde approach to option valuation, without the hassle of learning up Radon-Nikodým and martingales, I highly recommend this book!

| Best Sellers Rank | #952,224 in Books ( See Top 100 in Books ) #57 in Mathematics Reference (Books) #97 in Options Trading (Books) #150 in Probability & Statistics (Books) |

| Customer Reviews | 4.4 4.4 out of 5 stars (54) |

| Dimensions | 5.99 x 0.76 x 8.98 inches |

| Edition | 1st |

| ISBN-10 | 0521497892 |

| ISBN-13 | 978-0521497893 |

| Item Weight | 1 pounds |

| Language | English |

| Print length | 317 pages |

| Publication date | September 29, 1995 |

| Publisher | Cambridge University Press |

S**A

Five Stars

It's great as expected.

M**N

A good introduction to the PDE approach

Contrary to what many readers believe, this book explains the pricing of derivatives much better than Hull. Hull gives an overview of the mechanics and properties of the derivative pricing industry, along with its pricing methodologies, and this book provides an in depth method to one of the pricing methods. Financial derivatives can be priced by a wide range of methodologies, among some the elegant equivalent martingale measure approach (or risk-neutral pricing), replication, multinomial tree approximation, Monte Carlo simulation, partial differential equations etc etc. This book gives an excellent introduction, and an insight to the PDE approach. Although being a big fan of the Girsanov-change-of-measure method myself, these analytical methods often fail in the valuation of highly complex derivatives like the exotics. Pricing americans prove to be hard and inefficient too, even with simulation and the risk-neutral approach. This is where PDE methods come in. Since most derivatives (or term structures) have a PDE describing its evolution, solving the PDE seems to be a good (or sometimes the best) way, no matter how complex the derivative can get. PDEs on the other hand, have very robust and easy methods for solving. Therefore, this book brings the reader through basic PDE solving methods, analytical solutions, techniques for fast and efficient numerical approximations as well as rigorous technical explanations for some of the mathematics of partial differential equations (which arise in the financial industry). The authors are famous for their research in the field of Industrial and Applied Mathematics, and this book continues to be a classic for undergraduates in mathematics in Oxford. If you want to have an overview of the pde approach to option valuation, without the hassle of learning up Radon-Nikodým and martingales, I highly recommend this book!

C**.

good book

Good Book but it lacks lots of basic information to understand the material. In order to solve the problems, you will use more Google that the book if you are new to this area.

S**.

Good Book

I actually returned this book, but I have it now from somewhere else and the book is very helpful with math finance. There are good examples of how to work out each proof. It is just very helpful

H**E

Easy to read, very comprehensive.

I bought this book to learn about financial derivatives by myself. It is very easy to read for a first timer, no prior knowledge is required. It is also very comprehensive in its coverage of the subject. Overall it is a very good first book for the subject.

M**M

A Math Book that reads like an action novel

This books is certainly not for anyone. But if a person is interested in learning financial mathematics, it reads like an action novel. What I like about this book in particular is that it does not pound on theories with proofs after proofs. It just presents what one needs to know. Thumbs up!

M**G

A strong book, but not for the novice reader

The statement on the back this book that all the reader needs is some basic calc and a bit of probability is, as when you see it on most other similar books, false. To truly understand what is going on you need a prior knowledge of PDEs as well as some stochastic calculus. If you read this book after you have studies these you will learn a lot from it, but without this prior knowledge the book is too difficult to follow. I would recommend it to a reader who has seen the martingale approach to the subject before, and has at least studied ODEs and has a book on PDEs to refer to when the PDEs become too difficult to follow. The book manages to cover a lot, but you can't read a chapter and expect to have a good understanding from only reading the material. Most derivations, and even formulas, are left as exercises, and you need to complete at least 30% of the end of chapter exercises to firmly understand the material that the authors have covered. If you already have a good grasp of mathematical finance, this book can be a good way to further enhance your understanding, but don't buy this as an introductory book unless you are very strong in PDEs.

A**C

Finance with Differential Equations rather than Martingales

This is definite the best read for those who want a differential equations approach to derivatives rather than martingale methods. A good understanding of the "heat eaquation" is required. The book does the rest.

N**7

If you are doing any degree in quantitative finance, you must have this book on your personal library. I am doing an MSc in Quantitative Finance and this book is like the handbook for this kind of studies, I personally recommend this book if you want to improve your maths and programming skills.

A**R

really like a new book

E**K

Compré el producto en condición usado. Para el 85% de descuento en el precio respecto al de un producto nuevo, considero que fue una buena compra. Por ser de pasta blanda el libro presenta un doblez estructural. Se puede corregir poniendo debajo de algo que haga peso para plancharlo. Hay algunas manchas a los costados del libro, pero muy ligeras. Las hojas están intactas (salvó el doblez que mencioné) y solo la primera vino marcada con el nombre de su antiguo dueño. Mandándolo a empastar quedaría de lujo como un producto nuevo y, calculo, a la mitad de precio. Me siento satisfecho por el precio pagado.

K**S

Good enough condition. Still imminently applicable introductory text

B**R

I have always been fascinated by mathematical models that simulate real world activities. I am no mathematical genius although I hold an honours degree in Physics, so do have a nodding acquaintance with the nature of the random walk, and can handle partial differential equations to a fashion. The book is described as being useful for students intending to embark on a detailed module covering derivative products. In this sense it fits the bill perfectly. With just a passing interest I found the content to be quite readable and could follow the text with reasonable ease. It is however not a book for those who have not an inkling about the nature of randomness and statistical measures or who do not have any skill or knowledge of the calculus. Having said that, neither does one require a degree in mathematics to be able to understand the authors explanations of the Black Scholes equations. I would say an HNC or HND in old money or its equivalent in either maths or engineering would fit the bill. The authors do refer to a fair amount of mathematics with which one ought to be fairly familiar, but they also provide very good descriptions and explanations of derivative behaviour. Well recommended if you intending to take this for further study or just have a passing interest.

Trustpilot

3 weeks ago

2 months ago